Property Tax for Filer and Non-Filer in Pakistan (2026): Complete Investor Guide

Imagine a Tier-1 investor walks into your project sales office, ready to lock down a premium commercial floor or an entire block of high-end apartments valued at PKR 10 Crore (100 Million). The deal is structured, the installment plan is aligned, and the tokens are ready to change hands.

Then comes the compliance check.

If that investor is an un-filed entity, they will suddenly face an unexpected, multi-million rupee cash-flow shock at the registration stage. For real estate builders and corporate developers, tax status is no longer just a backend accounting chore handled by lawyers. Under the current tax regime, it is a critical variable impacting transaction velocity, project liquidity, and your overall client conversion rate.

The Federal Board of Revenue (FBR) has restructured the property tax framework to penalize undocumented capital. For developers targeting sustainable growth, understanding the active differences between a filer vs non filer is essential to protecting profit margins and closing high-value deals.

The Multi-Tier Matrix: Breaking Down the FBR Standings

To properly navigate transactions, developers must understand what is filer and non filer status in the eyes of the law. The FBR enforces a strict classification system where the literal filer and non filer meaning dictates your transaction costs:

- Active Filer: An individual or corporate entity that has filed their income tax returns on or before the official deadline. They appear cleanly on the active taxpayer list (ATL) and enjoy the lowest filer and non filer tax rates available.

- Late Filer: A Tier introduced to capture entities that missed the primary compliance deadline but filed later after paying an ATL surcharge. While they escape some total restrictions, they face intermediate, penalized tax rates on property transactions.

- Non-Filer: Legally, the non filer meaning applies to any entity completely absent from the ATL. In practice, being a non filer means facing aggressive withholding rates, banking transaction penalties, and operational hurdles designed to restrict non-compliant financial movement.

The structural difference between a filer and non filer status represents the line between profitability and stalled capital. When dealing with an investor who is a non filer in pakistan, a real estate business must immediately anticipate increased transactional friction. Choosing whether to proceed as a filer or non filer determines whether a deal closes smoothly or falls through due to unexpected overhead.

Advance Tax on Acquisition (Section 236K)

The statutory 236k tax governs the advance tax collected from the purchaser at the time of registering or transferring immovable property. This is where the cost of non-compliance hits a buyer’s immediate liquidity hardest.

While active filers pay a manageable base rate, the FBR applies a heavily scaled non filer tax penalty, which climbs significantly for higher-value luxury properties. This structural penalty heavily inflates the property purchase tax for undocumented buyers.

| Property Valuation Bracket | Active Filer Rate | Late Filer Rate | Non-Filer Rate |

| Below PKR 5 Crore | 3% | 6% | 12% |

| PKR 5 Crore to 10 Crore | 3% | 6% | 15% |

| Above PKR 10 Crore | 3% | 6% | 18.5% |

The Real-World Friction

When looking at the filer and non filer tax rates in Pakistan, the gap is staggering. Consider the financial impact on a commercial acquisition worth PKR 10 Crore under the current framework for tax on property purchase in pakistan:

- An Active Filer pays PKR 30 Lakh (3,000,000) in advance tax.

- A Non-Filer faces an 15% rate, requiring an immediate payment of PKR 1.5 Crore (15,000,000).

This steep non filer property tax creates a PKR 1.2 Crore cash deficit before construction or development even factors in. For developers attempting to calculate their property purchase tax in Pakistan to expand their project pipelines, purchasing as a non-filer locks up vital working capital that could otherwise fund structural materials or initial infrastructure.

Capital Gains & Selling Overhead (Section 236C & Section 37)

The tax burden is equally heavy on the exit side of a project. When a builder sells completed inventory, or when an investor flips a unit within a development, a distinct tax on sale of property applies under Section 236C (Advance Tax on Sale), followed closely by Section 37 (capital gain tax on property in Pakistan).

Advance Tax on Sale (Section 236C)

Collected from the seller during the transfer of immovable property, the tax on property sale in Pakistan is structured to encourage active filing status:

- Active Filer: 3% (Adjustable against final tax liability, rising to 4% for properties valued past 5 Crore).

- Late Filer: 6% to 9.5% depending on the property's valuation tier.

- Non-Filer: 10% to 11.5% flat across all values.

The Capital Gains Tax (CGT) Trap (Section 37)

For properties acquired after July 1, 2024, the fbr gain tax on property rules have eliminated the old exemptions based on multi-year holding periods.

The Rule: Active Filers pay a clean, flat 15% CGT on property in Pakistan on net profits, regardless of how long the property was held.

For non-filers meaning the absolute absence of a clean tax record, the profit is treated as normal taxable income and pulled directly into standard progressive income tax slabs. Depending on regional rules, such as the specific gain tax on property in Punjab or Sindh, this rate climbs rapidly, topping out at a punishing 45%. This dynamic effectively cuts an un-filed investor's net profit margin in half upon exit.

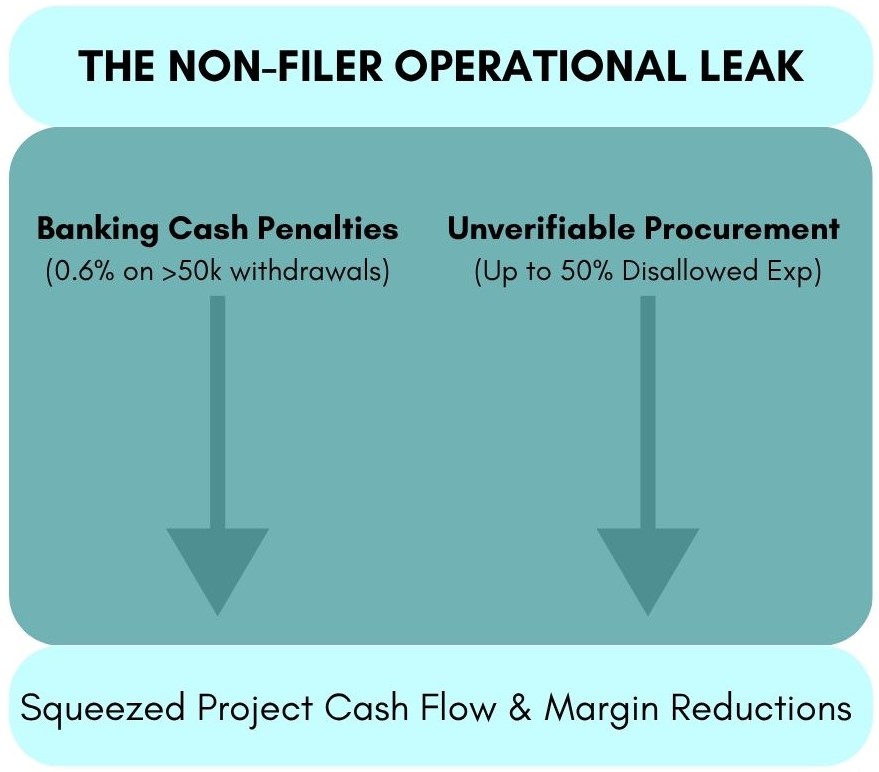

Corporate Builder Implications: Cash Flows & Supply Chains

Beyond client-facing transactions, a developer’s operational overhead is deeply affected by systemic compliance. Operating under an un-filed status introduces expensive hidden leaks across day-to-day operations through various FBR property tax components.

Banking Transaction Penalties

Large-scale construction relies heavily on fluid, day-to-day cash requirements—particularly for on-site daily labor payrolls and immediate vendor logistics. Non-filers are hit with a 0.6% withholding tax on all cash withdrawals exceeding PKR 50,000 in a single day. Over a multi-month construction cycle, this micro-tax accumulates into a noticeable operational loss.

The Procurement Trap

Under Section 21(s) of the Income Tax Ordinance, corporate developers who procure raw materials from non-filed vendors face severe penalties. Furthermore, regional development authorities are shifting completely to digital tax collection frameworks.

Whether you are trying to compute your liability using a property tax pakistan calculator, pulling a property tax calculator Karachi report, or attempting to settle an online property tax challan Sindh via the excise portal, integration with the FBR database is mandatory. Checking the property tax karachi online status will automatically reveal if your corporate entity is penalized. Failing to maintain active status means your provincial PT 10 challan or capital development authority property tax assessments in Islamabad will be processed under much harsher penalty slabs.

Leveraging Tax Literacy for Sales

Smart developers do not just complain about the fbr tax on property matrix, they use it to build trust, protect transactions, and drive sales velocity.

Deploy Compliance Advisories in Sales Teams

Instead of letting a non-filer client walk away due to sudden tax sticker shock, train your sales executives to act as structural advisors. By offering an in-house compliance path, guiding the buyer through the Iris filing process and transitioning them to the ATL before executing the final transfer deed, you save the buyer millions in upfront costs while securing the deal.

Transition Projects Toward Corporate and REIT Structures

To shield investors from personal tax volatility, institutional developers are increasingly utilizing Real Estate Investment Trusts (REITs). Land transferred to an FBR-registered REIT benefits from highly favorable capital gains tax exemptions and streamlined corporate tax treatments, making the underlying development units far more attractive to institutional capital.

Summary & Future Outlook

The FBR's regulatory trajectory indicates that the tax gap between compliant and non-compliant entities will continue to widen. The economic space for un-documented capital is shrinking, making a high property tax for non filer in Pakistan an expensive liability for both buyers and builders.

For Family Builders and Developers, maintaining clear documentation, working exclusively with compliant supply chains, and verifying the active tax status of your buyers are vital practices. By embedding tax literacy into your core corporate strategy, you protect your cash flows, minimize transactional friction, and position your brand as a secure partner for premium real estate investment.